U.S. Fed chair warns of more possible rate hikes but cites signs of economic cooling.

Anyone looking for firm direction from the world’s most powerful central banker in his much-anticipated speech on Friday in Jackson Hole, Wyo., will inevitably be disappointed.

Investors may be glad that U.S. Federal Reserve chair Jerome Powell did not use his 15 minutes in the global spotlight to crash the markets the way he did last year.

But taken literally, the Fed chair’s colourful statement that he is “navigating by the stars under cloudy skies” is a frightening reminder that as we head into the autumn, one of the world’s key economic leaders seems a little bit lost.

For more than 40 years, the people who ultimately decide how much you pay for your house and whether you will have a job next year have been putting their heads together at a stunning wilderness resort in Wyoming named after a local trapper from the 1800s, Davey Jackson.

Devoured by bears?

Rather than Jackson’s cabin, Powell and crew stayed at the luxury Jackson Lake Lodge during the three-day Jackson Hole Economic Symposium that ended on Saturday. But anyone even one-quarter as familiar with the outdoors as a 19th-century trapper will know that counting on travelling by the stars when they are obscured by clouds is a hopeless and even dangerous endeavour that could well leave you stranded in a swamp or devoured by bears.

Even as they donned checked shirts for their mountain escape from their normal habitat of skyscrapers and smog, it is only fair to say that Powell and his speech writers likely did not grasp how portentous their analogy would be to, say, an experienced Canadian hiker imagining being lost in the woods at dusk without a compass.

In many other portions of his short speech, Powell made it clear — as the Bank of Canada governor recently did even as he hiked interest rates — that the central bank remains flummoxed by conflicting data and that a false trail could lead us all in the wrong direction.

“Uncertainties, both old and new, complicate our task of balancing the risk of tightening monetary policy too much against the risk of tightening too little,” Powell told the Jackson Hole audience of central bankers, economists and financial reporters last week.

“Doing too little could allow above-target inflation to become entrenched and ultimately require monetary policy to wring more persistent inflation from the economy at a high cost to employment. Doing too much could also do unnecessary harm to the economy.”

Despite his fear of doing economic damage, Powell insisted that inflation was still too high and that the bank would raise rates again if it appeared core inflation was not getting back down to what he said still remains the central bank’s two per cent inflation target.

- Get the news you need without restrictions. Download ourfree CBC News App.

Conflicting data

The difficulty faced by Powell and his opposite number in Canada is that the data is all over the place.

The automobile sector, he said, was an area where a combination of a doubling in auto purchase loan costs and an end to supply chain blockages shows signs they are working together to bring inflation to heel.

“As the pandemic and its effects have waned, production and inventories have grown and supply has improved. At the same time, higher interest rates have weighed on demand,” Powell said. “Motor vehicle inflation has declined sharply because of the combined effects of these supply and demand factors.”

Specifically in the case of the United States, house prices and rents are showing signs of falling — but the slow pace of reduction may be one more example of the well-known lag effect, as interest rate impacts only slowly appear in the economy because they are still “in the pipeline,” he said.

“Because leases turn over slowly, it takes time for a decline in market rent growth to work its way into the overall inflation measure,” Powell said.

Canadians renters are also waiting for that slow process to emerge here, although intense housing demand north of the border may stand in the way.

In many other sectors, Powell said that any slowdown in price growth has been “modest” — and in jobs, consumer spending and rising gross domestic product, the bank sees signs that another hike in rates could be needed.

Higher for longer

Widely discussed last week and hinted at by Powell is the idea that interest rates could stay higher for longer as an alternative to more hikes.

Unlike Powell, Canadian economist Vivek Dehejia was able to put some real numbers on what kind of interest rates to expect. In a phone conversation, the associate professor of economics at Ottawa’s Carleton University suggested a path out of the woods is one where interest rates remain near their current levels until inflation approaches the central banks’ target.

Mortgage, food costs keep biting as inflation creeps up again

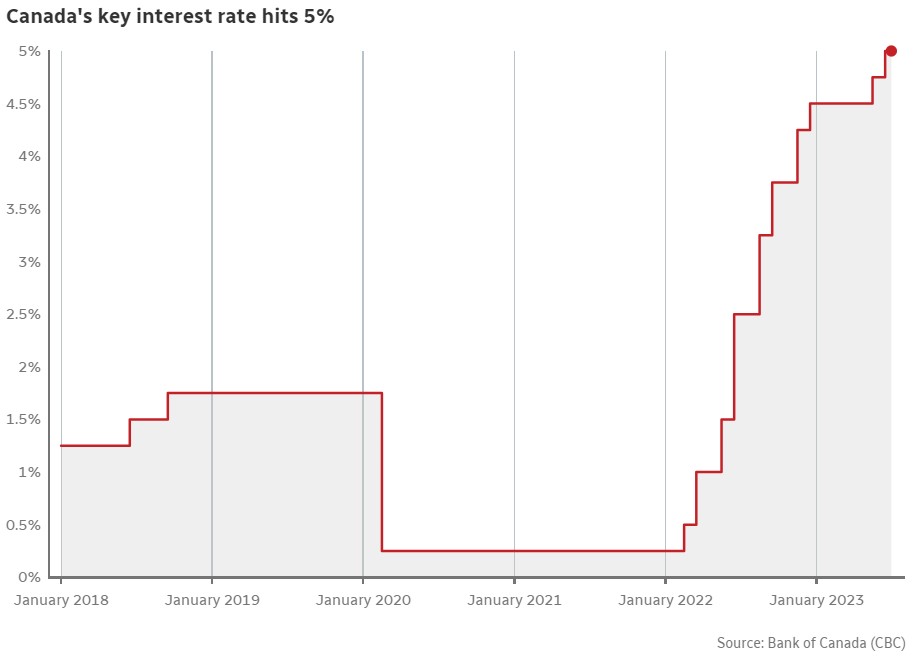

Canada’s overall annual inflation rate ticked up to 3.3 per cent in July, from 2.8 per cent in June. Homeowners now pay 30 per cent more in mortgage interest than 2022. And while food price increases dipped slightly from June, they’re still painfully high at 8.5 per cent over last year.

“Given that inflation seems to be trending down in both the U.S. and Canada, I think the more prudent course is to wait a bit, be a little patient and see what happens,” Dehejia said.

But he said he thinks that Canadian borrowers expecting interest rates to decline to the low levels near zero that pushed real estate prices to current heights are likely to be disappointed.

The fact is that over the longer term, central bank interest rates on both sides of the border average out closer to five per cent. Even after the current “restrictive” rate hikes are over, Dehejia expects rates to “normalize,” which will be in the three-to-four per cent range.

And then in the longer term, if the central banks should overshoot and put the economy into a deeper recession, Dehejia said, that would allow them to cut a little “because when you’re at or near zero, there’s no room to manoeuvre.”

As Powell stares up at the clouds and hopes for a glimpse of the stars behind, there is one sign he may be close to the right path. While some critics bashed his brief speech for moving us toward recession with higher rates, others worried he was too soft on inflation.

As Dehejia suggests, it is reasonable to think that until the economy shows its true direction with clues such as this Friday’s U.S. jobs data — Canada’s data is coming out on Sept. 8, too late to help Bank of Canada governor Tiff Macklem with his rate decision on Sept. 6 — the U.S. central banker will hold off on any policy rate decision until it proves necessary.

“This uncertainty underscores the need for agile policy-making,” Powell said.

ABOUT THE AUTHOR

Business columnist

Based in Toronto, Don Pittis is a business columnist and senior producer for CBC News. Previously, he was a forest firefighter, and a ranger in Canada’s High Arctic islands. After moving into journalism, he was principal business reporter for Radio Television Hong Kong before the handover to China. He has produced and reported for the CBC in Saskatchewan and Toronto and the BBC in London.

*****

Credit belongs to : www.cbc.ca