Moving beyond instant payments, the vision for seamless financial transactions involves the integration of digital assets, digital money, and digital infrastructure.

What if the problem is also the solution, and the solution is also the problem? Would that be a chicken-and-egg situation, or something akin to that adage, between the devil and the deep blue sea? That’s the conundrum that leaders of nations, as well as ordinary citizens, have to grapple with, if not now, certainly in the near future as the financial landscape undergoes a profound cross-border transformation.

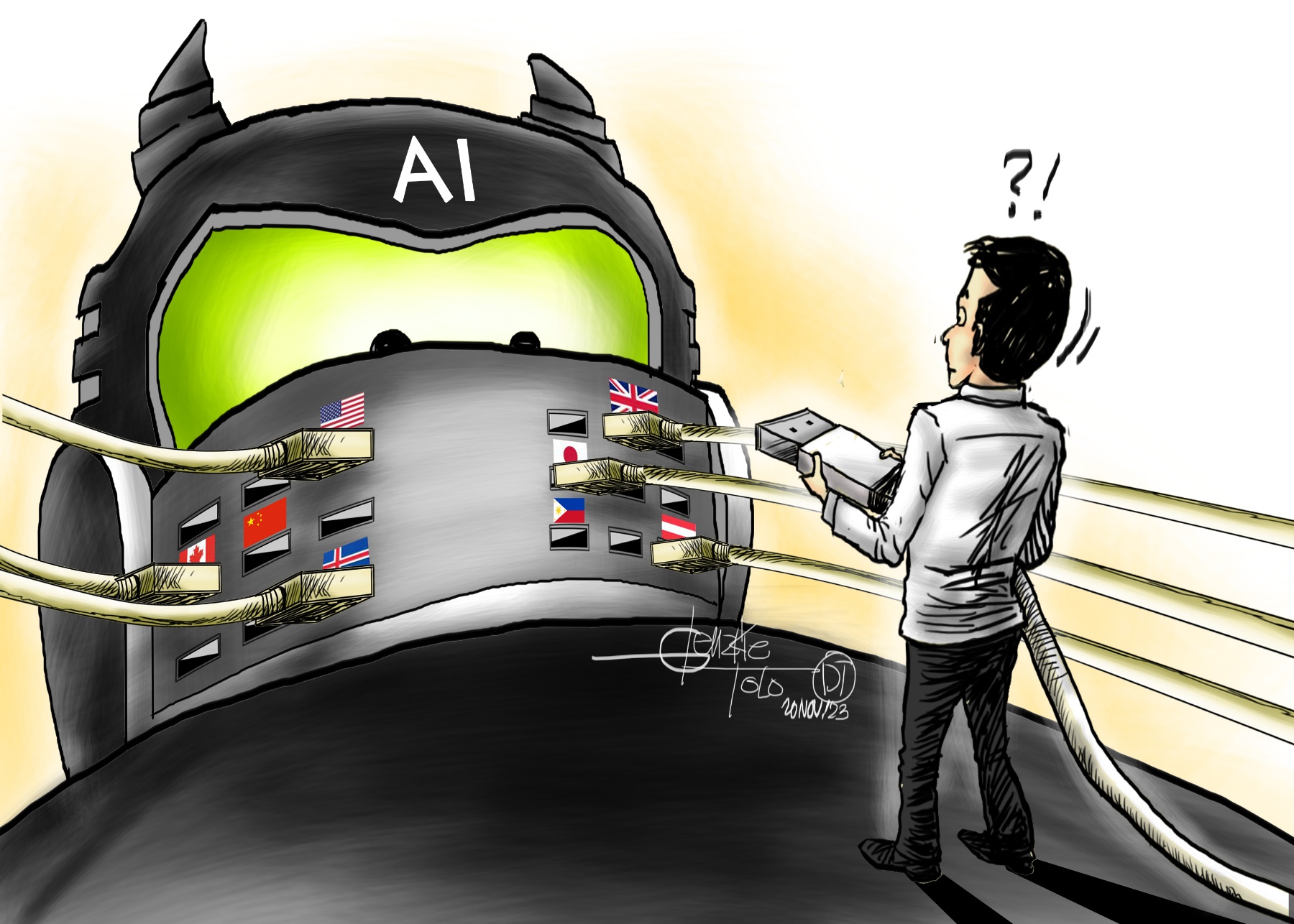

At the forefront of this evolution is the rapid progress of financial technology, or fintech, which is being powered and, at the same time, being assaulted by bad digital players using AI or artificial technology.

With e-payment at its heart, fintech has made it easy for someone visiting Japan or Singapore, for example, to finance their stay without needing local currencies like the yen or SGD. Credit cards? Too old a tech and too tedious.

One does not need to understand fintech to benefit from or use it. With a GCash tap card or similar cards issued in the Philippines, one can buy soda from a vendo machine, a train ticket, lunch, or anything else in Tokyo.

While the monetary value or load on the card may be in Philippine pesos and the transactions are in yen, the currency conversion is done automatically, and the customer experience at points of sale can be hassle-free most of the time.

Tap this and tap that, and after every transaction, your card issuer in the Philippines buzzes you on your smartphone about how many pesos you still have. Replenishing the cards is as easy as loading them through online banking.

A year ago, the Monetary Authority of Singapore outlined five fintech targets — instant remittance, atomic settlement, programmable money, tokenized assets, and trusted environmental, social, and governance data.

Appearing via hologram to keynote the 2023 Singapore Fintech Festival last 15 November, President Ferdinand Marcos Jr. revealed that private-public sector partnerships are being undertaken to transform the Philippines into a financial technology hub. If only because Singapore has already emerged as the global leader in the e-payments domain, the Philippines will have plenty of catching up to do.

Singapore’s evolution from domestic transfers to bilateral linkages and now multilateral networks showcases its commitment to making cross-border payments cheaper, faster, and more efficient. The retail payments infrastructure, including FAST and PayNow, has democratized digital transfers, allowing individuals and businesses to transact in real-time, 24/7, and at zero cost.

Likewise, the success of Singapore’s QR code-based mobile payments, exemplified by the SGQR label, is simplicity itself. This single label, accepted by over 90 percent of merchants, has simplified transactions for consumers and set the stage for complete QR interoperability with the upcoming SGQR+. This innovation allows merchants to consolidate transfers from various payment schemes, streamlining financial operations.

And Singapore’s leadership extends beyond its borders as it has already established bilateral payment linkages with countries like Thailand and India, and soon with Malaysia. QR payment linkages with China, Malaysia, and Thailand have facilitated seamless transactions for travelers. The upcoming connectivity with Indonesia’s QRIS demonstrates the expansion of these regional collaborations.

Moving beyond instant payments, the vision for seamless financial transactions involves the integration of digital assets, digital money, and digital infrastructure. Tokenization, a critical feature of digital assets, enables direct exchange and fractionalization, paving the way for atomic settlement and broader investor access.

Back in the Philippines, hardly one card can be used in nearly all transactions. The railway systems use different tap cards, and motorists are saddled with securing other RFID stickers passing through tollways. With companies unable or unwilling to be under a singular umbrella, Filipinos may still be years away from the interconnectivity many other Asian countries have already rolled out to make e-wallets work the way they are intended through AI-powered fintech.

But as AI and fintech make financial transactions easier in a post-pandemic world, it is crucial to acknowledge the challenges accompanying these advancements, including the potential for exploitation by hackers, necessitating robust cybersecurity measures.

Here is where the one-upmanship game between fintech movers and bad players in the underbelly of the digital world becomes critical as both use AI to either power or defeat systems. For hackers, fintech has made the attack surface even bigger as every inter-connection is a potential entry point for an attack. If the full potential of fintech and e-payments is to be realized on the world stage, nations must commit to collaborate, especially on cybersecurity.

It is not about one country like Singapore or Japan leading fintech innovation because interconnectivity is the objective, the same interconnectivity that local players in the Philippines, notwithstanding a push by the government for such, cannot seem to get their heads together to accomplish.

*****

Credit belongs to: tribune.net.ph